Angst over economic rankings is usually whipped up by public sentiment as economies are an aggregation of households and behaviourally take after their gregarious nature or desire for alignment with peers.

There is an urge to see one’s home country measuring up to peers on every metric, if not superseding the peer group benchmark. This is the source of dysphoria from having Zimbabwe as an unrated sovereign among rated neighbours in Sub Saharan Africa when core economic fundamentals tag along very well. Using the IMF World Economic Outlook database, October 2023, Zimbabwe’s GDP per capita fares well relative to peer Sub-Saharan African countries.

Compared to a selection of 20 peers and the Sub-Saharan African average, Zimbabwe’s GDP per capita is in kilter with lower middle-income peers and projections over the forecast period to 2028 show a superior trend.

Unfortunately, the level of domestic competitiveness reflected in GDP per capita trends is not being projected at international level when plotted against sovereign ratings. While sovereign ratings are not entirely dependent on GDP per capita, a strong positive correlation between average national household income and credit quality steps is demonstratable. Sovereign rating models normally have multiple variables, with Fitch Ratings Standard Rating Model “employing 18 variables based on three-year centred averages, including one-year forecasts”.

In this respect, divergencies between GDP per capita metrics and credit quality steps usually arise from other factors, like governance weaknesses, measured using the World Bank Governance Index, public debt to GDP ratio, public finance management, economic growth, access to reserve currencies, external account management, a kitchen sink of competitiveness factors and other adjusters. Other rating agencies have similar models to Fitch, either in structure or outcomes, given the high correlation in sovereign ratings from the three leading rating agencies across the ratable universe.

Notwithstanding the interplay of multiple variables, GDP per capita drives the core rating, hence countries that sustainably uplift income per capita are likely to experience an upward progression in sovereign ratings over time. Using GDP per capita and assuming a neutral assessment on other factors, Zimbabwe’s sovereign rating theoretically falls within the ‘B’ range as shown using peer comparatives below.

A ‘B’ rating under Fitch rating definitions implies that “material default risk is present, but a limited margin of safety remains. Financial commitments are currently being met; however, capacity for continued payment is vulnerable to deterioration in the business and economic environment”.

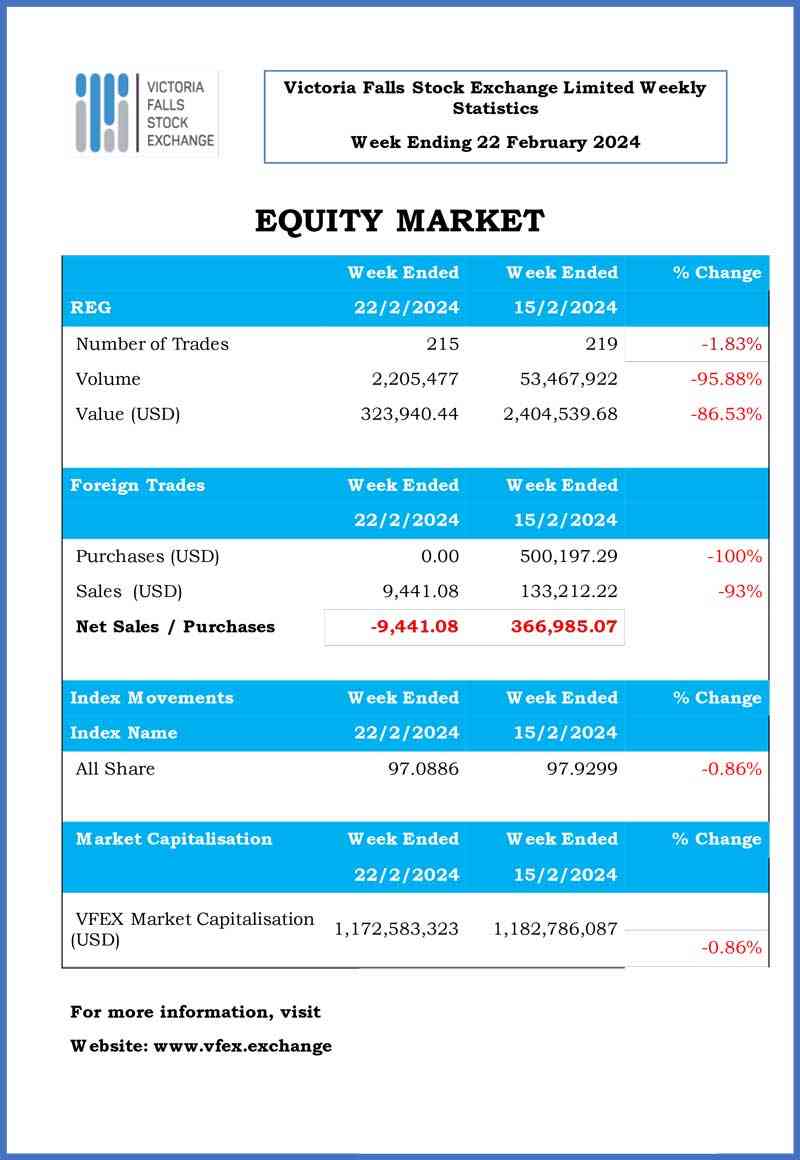

- Legacy debt hindering Zim return to world market

Keep Reading

An anchor credit rating of ‘B’ places the country in the same cohort with Kenya, Tanzania and Rwanda. The other factors that explain sovereign ratings will determine whether Zimbabwe can hold the anchor rating or migrate lower. Kenya evidences a higher GDP per capita of $2,187, while Rwanda ($1,031.69) and Tanzania ($1,326.63) have significantly lower GDP per capita.

Kenya’s Achilles’ heel is the high general government gross debt to GDP ratio of 70% (2022: 68%) with the fading spectre of default on upcoming Eurobond bullet maturities having placed the sovereign rating on downgrade watch. Fortuitously, the East Africa hub economy had a successful issuance of a US$1.5bn Eurobond on 12 February 2024, which was oversubscribed, receiving US$5bn bids, and proceeds are earmarked to settle part of the June 2024 US$2bn Eurobond maturity. The new bonds have a maturity period of 7 years. According to Bloomberg, the clincher to the default avoiding deal was the pricing, which came out high at 10.375%, exceeding rates for recent issuances by Benin (8.375%, 14-year instrument) and Ivory Coast (two bonds of 9 and 13 years priced at 6.30% and 6.85% respectively).

On the other hand, low GDP per capita levels for Rwanda and Tanzania receive uplift from positive assessments on institutional and fiscal strengths respectively.

Using the Worldwide Governance Indicators, Rwanda is one of the few African countries with a positive assessment on control of corruption, rule of law, regulatory quality, government effectiveness and political stability and no violence.

The landlocked East African country only stoops to a negative estimate on the voice and accountability.

On all these indicators, estimates for Tanzania and Kenya are negative and Zimbabwe flirts with bottom rankings, mostly at below negative 1.

Rwanda’s strength is moderated by a debt to GDP ratio of 61.1% and the backdrop of a low GDP per capita. However, neighbouring Tanzania boasts of fiscal discipline as evidenced by a debt to GDP ratio of 42.6% (2022: 42.3%), which can provide rating uplift under some models. Fundamentally, high debt to GDP ratios are normally not a major issue if other economic drivers render debt sustainable; for instance, when the country’s GDP is growing at a fast rate and a large portion of the debt stock is domestic or concessionary.

Rwanda’s fast-growing economy at a projected steady state growth of 7.2% over the next five years is positive, as well as corresponding projected real GDP growth rates of 5.3% and 6.6% for Kenya and Tanzania, respectively. On the other hand, IMF estimates Zimbabwe’s debt to GDP ratio at 95% in 2023 and real GDP growth is projected at a neutral 3.34% over the next five years.

In this respect, strong growth among East African countries can give the cohort a rating uplift, while growth remains neutral to Zimbabwe. Furthermore, a very high debt to GDP ratio, which is a significant rating negative, increases divergence below the benchmark.

Given the above profile of sovereign ratings’ drivers, the theoretical core sovereign rating for Zimbabwe adjusts downwards from a ‘B’ range. The negative adjusters stem from negative scores on the Worldwide Governance Indicators and a high debt to GDP ratio, while real GDP growth can be classified as neutral. Using this limited set of factors, the adjusted theoretical sovereign rating reduces into the CCC band, implying “very low margin of safety, default is a real possibility” on Fitch’s rating scale.

Of course, that would be a partial analysis as one has to consider whether the country is in default or not. A default to some creditors brings the sovereign rating to an ‘RD’ implying “the issuer has an uncured payment default or distressed debt exchange…but has not otherwise ceased operations”.

This economic mire must be avoided, and Zimbabwe must work its way out of the ditch. The big considerations are;

Whether the factors suppressing Zimbabwe’s sovereign ratings cannot be remedied;

If they are remediable, how long can it to take to improve competitiveness, and restructure debt with creditors, as these long standing issues are achievable but remain evasive; and

To what extent can Zimbabwe dial up drivers such as GDP per capita and competitiveness to offset structural issues such as governance?

Ostensibly, countries with law voice and accountability scores like Rwanda and Saudi Arabia balance such weaknesses with positive scores on rule of law and control of corruption within the governance index to ameliorate the overall outcome.

The undesirable state of being a laggard on all sub-factors on governance requires concerted efforts to manage and shape a better trajectory going into the future. A strong resolve is also needed to reach a settlement with lenders on the back of sound policies in a transformative manner as proposed by the 2010 IMF team headed by Vitaliy Kramarenko in a timeless report titled ‘Zimbabwe: Challenges and Policy Options after Hyperinflation’, asserting that mining wealth (even by mortgaging future fiscal revenue from mining) and non-mineral surpluses will not generate sufficient resources to settle international arrears.

The quick and viable option is debt relief negotiations to redeem Zimbabwe from a default status and align the sovereign rating with the core level of ‘B’ as indicated by GDP per capita — the most important structural factor. Most importantly, a realisation that most of the debt (and interest arrears) is an intertemporal injustice to generations that have little connection with the original purpose and use of the debt should motivate a write-off. The prospect of Zimbabwe issuing $5bn debt on international markets at interest rates of below 7% p.a., given high returns in agriculture and mining would reset the country on a highly transformative economic journey.

- Chingono has experience in credit analysis focusing on insurance companies, banks and corporates. He is currently a credit analyst based in Australia and founder of ratings advisory business, Quad P Investor Services. — [email protected].